Things about Mortgage Investment Corporation

Things about Mortgage Investment Corporation

Blog Article

Mortgage Investment Corporation Things To Know Before You Buy

Table of ContentsThe Best Strategy To Use For Mortgage Investment CorporationUnknown Facts About Mortgage Investment CorporationThe 30-Second Trick For Mortgage Investment CorporationThe smart Trick of Mortgage Investment Corporation That Nobody is Talking AboutIndicators on Mortgage Investment Corporation You Should Know

Does the MICs credit rating committee evaluation each home mortgage? In the majority of situations, home loan brokers manage MICs. The broker ought to not function as a participant of the credit committee, as this puts him/her in a straight problem of interest considered that brokers typically make a commission for putting the home loans. 3. Do the directors, members of credit rating board and fund supervisor have their very own funds invested? A yes to this question does not give a safe investment, it ought to provide some raised protection if examined in conjunction with various other sensible financing policies.Is the MIC levered? Some MICs are levered by a banks like a legal bank. The economic organization will certainly accept particular home loans possessed by the MIC as safety and security for a credit line. The M.I.C. will certainly then obtain from their line of credit report and lend the funds at a greater price.

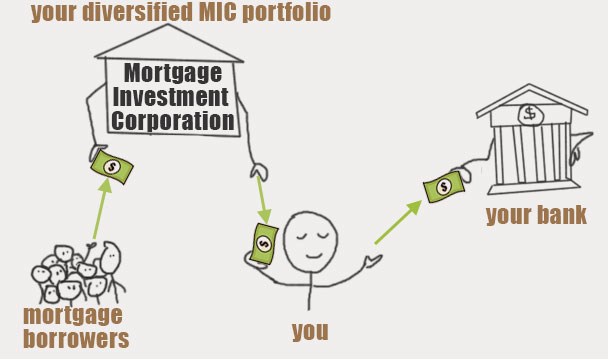

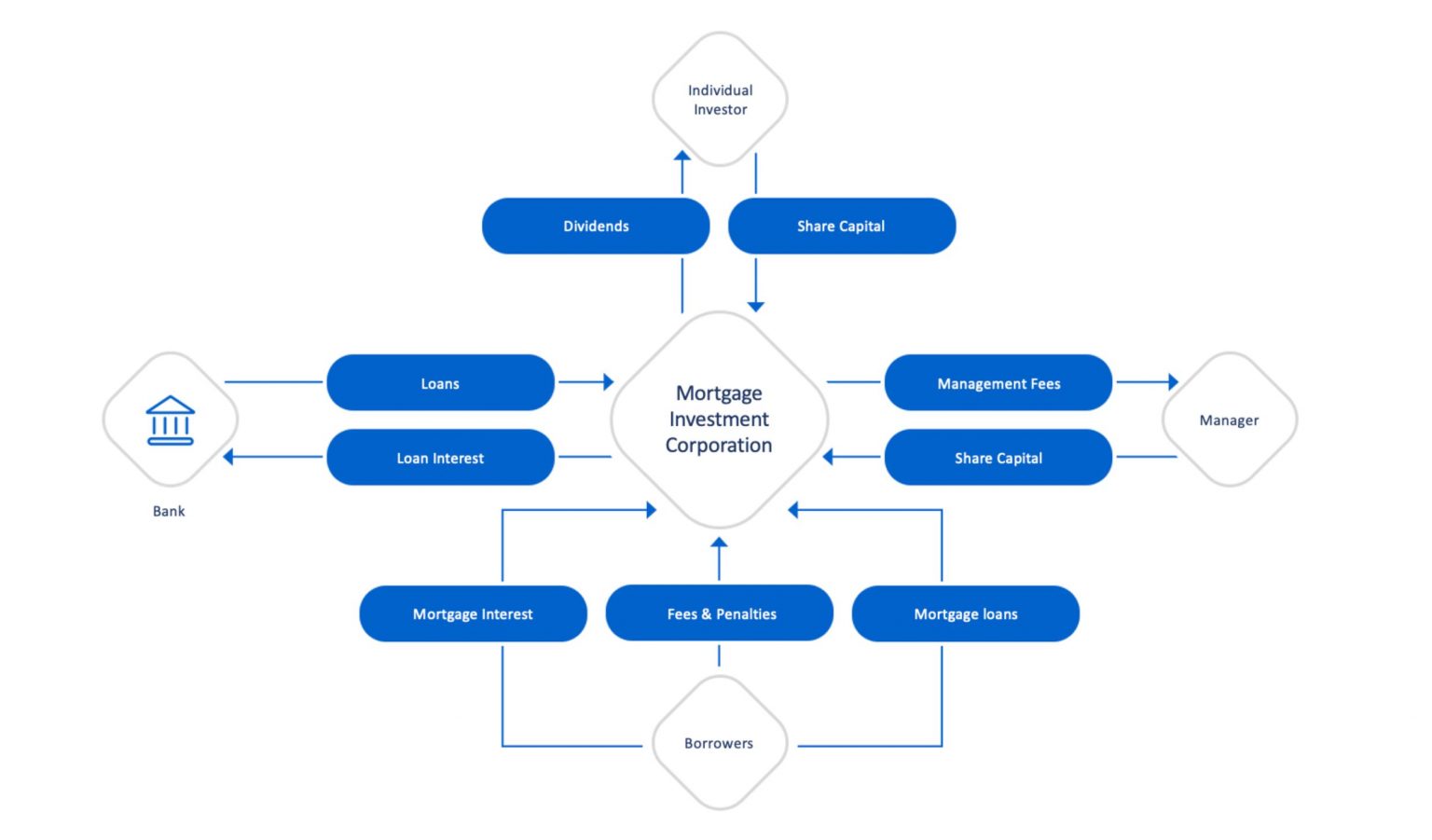

Last upgraded: Nov. 14, 2018 Few financial investments are as advantageous as a Home mortgage Investment Firm (MIC), when it pertains to returns and tax advantages. Due to their corporate framework, MICs do not pay income tax obligation and are legally mandated to disperse all of their incomes to investors. In addition to that, MIC dividend payouts are dealt with as rate of interest revenue for tax objectives.

This does not imply there are not dangers, however, normally talking, no issue what the more comprehensive securities market is doing, the Canadian realty market, specifically significant city areas like Toronto, Vancouver, and Montreal carries out well. A MIC is a corporation formed under the guidelines lay out in the Income Tax Act, Area 130.1.

The MIC gains revenue from those home mortgages on passion fees and general fees. The real appeal of a Home mortgage Financial Investment Firm is the yield it offers investors compared to various other set earnings investments - Mortgage Investment Corporation. You will have no trouble finding a GIC that pays 2% for a 1 year term, as federal government bonds are equally as low

8 Easy Facts About Mortgage Investment Corporation Described

A MIC must be a Canadian company and it have to invest its funds in home loans. That claimed, there are times when the MIC finishes up owning the mortgaged residential property due to repossession, sale agreement, etc.

MICs problem common and recommended shares, issuing redeemable favored shares to read more shareholders with a taken care of dividend price. These shares are considered to be "certified investments" for deferred revenue plans. This is suitable for investors who acquire Mortgage Investment Corporation shares via a self-directed registered retirement cost savings strategy (RRSP), registered retirement earnings fund (RRIF), tax-free financial savings account (TFSA), look at here deferred profit-sharing plan (DPSP), signed up education and learning savings plan (RESP), or registered impairment savings plan (RDSP)

Unknown Facts About Mortgage Investment Corporation

And Deferred Plans do not pay any type of tax on the rate of interest they are estimated to receive. That said, those who hold TFSAs and annuitants of RRSPs or RRIFs may be struck with particular fine tax obligations if the financial investment in the MIC is taken into consideration to be a "banned financial investment" according to Canada's tax obligation code.

They will ensure you have found a Home loan Investment Company with "certified financial investment" standing. If the MIC certifies, maybe very advantageous come tax time because the MIC does not pay tax on the rate of interest earnings and neither does the Deferred Plan. Much more generally, if the MIC stops working to fulfill the needs established out by the Earnings Tax Act, the MICs earnings will be exhausted before it obtains dispersed to investors, reducing returns substantially.

Much of these dangers can be reduced though by talking to a tax obligation professional and financial investment representative. FBC has worked exclusively with Canadian local business proprietors, business owners, capitalists, ranch operators, and independent specialists for over 65 years. Over that time, we have helped 10s of hundreds of clients from across the nation prepare and submit their taxes.

Some Known Factual Statements About Mortgage Investment Corporation

It shows up both the real estate and stock markets in Canada are at all time highs At the same time yields on bonds and GICs are still near record lows. Even cash money is shedding its appeal since power and food prices have pushed the inflation rate to a multi-year high.

If passion prices climb, a MIC's return would certainly additionally raise due to the fact that greater home mortgage prices suggest even more earnings! MIC financiers just make money from the enviable position of being a lender!

Lots of difficult working Canadians that desire to purchase a house can not obtain home loans from conventional banks due to the fact that probably they're self utilized, or don't have a well-known credit rating background. Or perhaps they desire a brief term funding to establish a large building or make some improvements. Banks tend to neglect these prospective borrowers due to visit site the fact that self utilized Canadians do not have steady incomes.

Report this page